A prudent man foresees evil and hides himself, but the simple pass on and are punished.

Proverbs 22:3

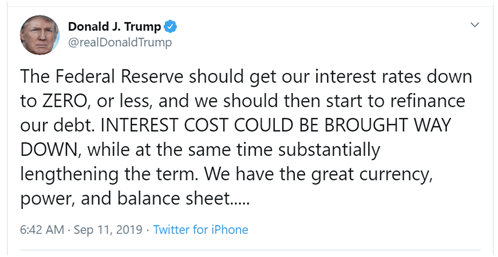

When I began writing this series back in early August, I did so as a response to a hard selloff in the stock market that followed the Fed’s decision at the end of July to lower interest rates. As I noted in that first post in this series, I decided on the title “The Ongoing Financial Crisis of 2008” because it is my view that the market melt down that began in earnest in the fall of that year has never really gone away.

What occurred was that central banks took money printing into hyper-drive in late 2008 and early 2009 and managed to reflate the stock market bubble that had popped earlier in 2008. I likened their actions to what the prophet Ezekiel called plastering walls with untempered mortar. In other words, the Fed addressed the symptoms of the financial crisis, but not the cause of the crisis itself.

Eleven years later, this is still the case. Nothing has been fixed. Nothing has improved. In fact, not only have things not improved, they have gotten far worse.

The 2008 crisis, what is sometimes called the Global Financial Crisis or the GFC, was a debt crisis. There was simply more debt in the financial system than could be repaid. So what was the response of the Fed and the federal government? They conspired to create even more debt to solve a crisis caused by too much debt, as if somehow more of the same thing that caused the problem in the first place was also the solution!

To borrow an English proverb, this was the financial equivalent of bringing coals to Newcastle.

If a man is an alcoholic, you don’t cure hm by giving him another bottle of whiskey. While another bottle may make him feel better for the moment, in the long run it will kill him. Yet this is not so very different from what governments and central banks all over the world did in 2008. They went on a spending and money printing spree, which managed to kick the can down the road but did nothing to solve the underlying problem.

As a result, while the economies of the United States and other Western nations have appeared to recover their health, the underlying fundamentals of those economies have grown steadily worse. Just in America, our national debt has more than doubled since 2008 and now sits at $23 trillion.

Just to give you as sense of how fast debt is now piling up, it took the federal government from the founding of our country until 1982 to compile $1 trillion in debt. Now, even mainstream sources are predicting that the annual deficit for fiscal year 2020 – this is the federal government’s fiscal year which began on October 1, 2019 and ends on September 30, 2020 – will be in excess of $1 trillion. In other words, the federal government is adding the same nominal amount of debt in a single year that it previously took about 200 years to accrue.

Oddly, no one in Washington seems the least bit concerned about this. Not the Democrats. Not the Republicans. No one except an odd fellow here and there such as Senator Rand Paul.

The Bible teaches us that debt is a burden. At best, it is something that is to be used prudently and paid off timely.

Yet we all live with a debt-based financial system that, not only encourages debt, but actually requires debt to increase at a faster and faster pace just to keep the system from imploding. This debt-based system of financial perdition was put in place in the United States with the passing of the Federal Reserve Act of 1913. The Fed has been destroying not only the financial fabric of the nation, but its moral fabric as well, for over 100 years.

What is true of America is also the case with all other Western nations.

We have become enslaved by debt, and all the more with each passing year.

But just as untempered mortar quickly shows itself when exposed to a little rain, so too are the phony fixes put in place in 2008 beginning to come unglued. In fact, this author has been amazed by how badly the financial system has deteriorated in the past three months he has been writing this series.

In just that short time, the Fed has, apparently on a permanent basis, started baling out the overnight repo market, twice cut interest rates and resumed Quantitative Easing (QE). These are all various forms of money printing, which have the long-run effect of weakening the dollar resulting in higher prices and a lower standard of living.

And these are just the activities they openly acknowledge. In the opinion of this author, the Fed rigs all financial markets 24/7 to provide the appearance of normalcy. Stocks, bonds, real estate and oil are propped up, while precious metals – gold and silver – and crypto currencies are suppressed.

Bet even as the Fed rigs all markets and the government statisticians put out phony economic numbers designed to understate unemployment and inflation while overstating economic growth, there are some stats that cannot be rigged.

If one looks closely at the economic numbers that are put out, he will see that, all the economic cheer leading from the administration aside, there is almost no good economic news to be found. Here is just a sample of recent headlines showing just how serious things are getting:

- “U.S. leading indicators fall for third straight month, adding more evidence of slowing economy”

- “U.S. labor market slowing; manufacturing mired in weakness”

- “Recession Warning: Freight Volumes Negative YoY For 11th Straight Month”

- “Trump Promises Farmers More Aid Amid Plunging Incomes”

- “Americans now have a record $14 trillion in debt”

- “US Industrial Production Plunges Most Since March 2009”

- “US retail sales unexpectedly decline in a sign that the consumer economy could be cracking”

I could easily produce many more such headlines, but I trust the reader gets the point that, economically speaking, things aren’t all that great out there. What’s even more remarkable is that these headlines are showing up at a time when the Fed has put the money printing pedal to the metal, intervening more aggressively in the market than at any time since the height of the 2008 crisis.

But while all that money printing has, apparently, not turned around the economy, the stock market is hitting new record highs.

So which is it? Are we to believe, the stock market, the politicians and the Wall Street cheer leaders, who tell us everything is awesome, or the economic statistics which point to an oncoming recession?

For my part, I’ll trust the economic statistics. Not, mind you, because I think economic statistics furnish us with knowledge. Only the 66 books of the Bible do that. No, it’s not that economic statistics are true that causes me to trust them. Rather, it is that the monetary and fiscal policies pursued by central banks and Western governments – that is to say, money printing and deficit spending – are morally bankrupt and will, in the long-run, inevitably lead to financial bankruptcy as well.

All this naturally leads to the question, when will the next economic crisis hit? My answer: I don’t know.

In my opinion, the entire world economic system should have collapsed in 2008, but extraordinary action by the world’s central banks managed to resuscitate the system. The financial system could easily have collapsed any time since then, but for the ongoing interventions – both public and secret – of central banks and governments ever since.

In short, we’ve all been living on borrowed time.

So how much more time are the masters of the universe able, or even willing, to buy? I don’t know.

In my opinion, the apparent quickening pace of the slide into recession seems to indicate that the time before the next major financial crisis is relatively short. That said, this author has been amazed at the ability of the establishment to maintain order as long as they have, so I would caution against any predictions that the wheels are definitely going to come off in the short-term. Quite obviously, the Trump administration is doing everything in its power to maintain normalcy until after the November 2020 elections, which are just under a year away. Can they hold things together until then? We’ll see.

But regardless of the timing, it is my thesis that a major financial crisis is coming. This will not be a garden variety recession. It will be like the 2008 crisis, only worse, for the simple reason that the debt crisis has gotten worse. Instead of dealing honestly with things in 2008, all we did was double down on the debt and kicked the can down the road.

But the point is coming when the can is no longer kickable.

That’s when things will get interesting.

And that’s the reason I’ve written this series on prepping. The bill for our debts is coming due, and I have a great burden to alert my fellow Christians to this, so that they may, as the prudent man in Proverbs 22:3, foresee trouble coming and hide themselves.